Commentary

Yezid Sayigh

Source: Getty

The armed forces champion a form of capitalism that is generating revenue, but its reliance on rent faces diminishing returns, leaving the country with massive sunk costs and deferred returns, deepening dependency on external borrowing.

Egypt’s emphasis on publicly funded construction under military management has consolidated into “landlord capitalism,” based on deriving rent from managing and monetizing state assets rather than from producing goods and services. This may indicate maturation in producing surpluses in a few economic sectors, potentially enabling expansion in others. But it may also point to saturation, as the military’s mechanisms of extraction of rent are approaching inherent limits, while deepening dependency on external borrowing.

The role of the military in the Egyptian economy has expanded and evolved continuously since the armed forces took power in 2013, and especially since former defense minister Abdel-Fattah al-Sisi assumed the presidency the following year.1 Three broad factors have driven this trajectory. First was Sisi’s immediate desire upon assuming office to portray Egypt as ready for business, in order to attract foreign investment and other inflows of capital. Second, he has sought unceasingly to generate state revenue for a depleted treasury, above all by monetizing state assets through private investment. Third, his faith in the superior administrative skills, discipline, and political loyalty of the armed forces prompted him to assign an ever-widening swath of activities in an expanding set of economic sectors to military management.

Having grown dramatically in scope and scale until 2020, the military’s economic role has since undergone a qualitative shift in both mode and organization. Most prominently, the heavy emphasis in the 2014–2019 period on publicly funded construction under military management has consolidated into what can be called “landlord capitalism,” a form of state capitalism based on deriving rent from managing state assets rather than from producing goods and services. An accompaniment to this shift has been the rise of military “champions”: agencies belonging to the Ministry of Defense or the armed forces that have won presidential favor and, as a consequence, have been awarded a greater share of military-managed economic ventures in return for their perceived success in monetizing state assets, primarily state-owned urban real estate and desert land. The qualitative shift has been partial, however. Other military agencies that operate through roughly a hundred formally registered military companies that engage in commercial activities have maintained business as usual in their sectors, such as manufacturing, retail trade, mineral extraction, and services. These companies form a residual part of the military economy. They act mainly as vehicles for patronage and elite circulation within the armed forces, rather than as important drivers of the economy as a whole.2

Has the military economy reached a stage of maturation, in which it is more effectively organizing the means of generating financial surpluses in a few economic sectors, and enabling potential expansion in others? Or has it entered a stage of saturation, in which both its traditional and its novel mechanisms of extraction of profit and accumulation of wealth have reached, or are approaching, inherent limits, while becoming ever more dependent on external borrowing? The shifts in the military economy point to a core tension: Its fundamental configuration as a system in which political and coercive power are directly convertible into economic accumulation hinges entirely on maintaining a national debt trap that generates recurrent needs to obtain foreign currency, service external obligations, and secure periodic bailouts. Sustainability therefore depends only partially on improved economic performance, and far more on geopolitical alignments ensuring continued capital inflows. Consequently, structural lack of competitiveness, macroeconomic crises, and bailouts leave Egypt vulnerable to external shocks.

The evolutionary pattern of the military economy reflects how it functions within a power structure in which the president is both paramount and, at the same time, wholly dependent on the institutional support and political loyalty of the armed forces. The same applies to the military’s integration into the political economy of production, management, and capital formation. On the one hand, the armed forces are a full institutional partner, but Sisi enjoys overall authority in setting the direction and prioritizing forms of state-led investment under military management. On the other hand, while there is complete identity of economic vision and assumptions between Sisi and the military, their relationship is also interest-based, constraining his autonomy and at times compelling him to compromise or delay on certain issues.

More broadly, despite the primacy of the president and military, other market participants, including civilian government economic authorities, state-owned enterprises, and the private business sector, also have agency. While these other participants in the market are constrained to a significant extent by a power structure in which they have limited political say, they continue to function in set ways within their remits and sectors and defend their own institutional and economic interests. This reflects what political economist Amr Adly has labeled Egypt’s “cleft capitalism”—a rentier system characterized by poorly integrated markets, a segmented private sector, and the relative lack of coherence and coordination among state bureaucratic actors.3 The military economy arguably reveals its own version of cleft capitalism, as the coexistence of new and residual modes characterized by divergent levels of competence, efficiency, and administrative capability reflects the central imperative of maintaining a rentier system.

Crucially, although the private sector accounts for an estimated 75 percent of gross domestic product (GDP), the International Monetary Fund has assessed, “The economic landscape is dominated by public-driven investments, an uneven playing field, and state-owned entities, including military ones, that operate directly in product markets.”4 Advantages for civilian state-owned enterprises and other government bodies involved in the economy have diminished, especially after Law 159 of 2023 formally ended their tax exemptions. However, the law’s real impacts remain ambiguous, and in any case military-related entities remain exempt.5 State entities crowd out the private sector, including for credit in a banking system in which approximately two-thirds of all assets are held by state-owned banks.6 And because public spending accounts for three-quarters of all investment, with infrastructure in particular absorbing 45–60 percent of total public investment, the state is an important source of contracts for large and medium private enterprises.7

Egypt’s political economy is evolving nonetheless, albeit in ways that do not converge or align. New niches of (mainly) private-sector activity are appearing, such as the employment of a growing number of businesses and skilled labor on behalf of Gulf firms investing in Egypt. Younger middle class customers seeking to preserve the value of savings amid the constant risk of high inflation are generating a surge in users of retail investment apps such as Thndr, and in registrations on the Egyptian stock exchange.8 Large real estate developers are following in the military’s wake, investing heavily in private new cities and resorts for upmarket customers. As the latter example in particular shows, some of these private-sector activities coexist with enduring modes of doing business that, despite some adaptation to evolving market conditions and technological developments, still reproduce classic patterns of rentierism: the generation of income through control of key assets such as land or of the award of public contracts, rather than through productive work, technological upgrading, or market innovation. This helps explain Egypt’s poor integration into global value chains.9

The military economy is no different. A few military agencies follow new business models and organizational modes—albeit also with a strong rentier element—while the remaining military agencies and companies maintain legacy forms that are noticeably less productive and efficient. This was evident in the first years of Sisi’s presidency, as the urgency he imparted to his economic and reputational goals inadvertently generated a wasteful free-for-all as multiple military agencies launched business activities for which they were ill-suited, duplicating projects and activities in the same sectors.10 The fact remains, however, that both the new and the legacy modes are enabled by the structure within which the Egyptian economy functions, but are also constrained by it. On one side is the preponderant power of the state to set direction and drive market activity through incentives and its investment strategy, which, on the other side, requires the state to continually manage its debt dependency and repeatedly secure access to foreign currency.

Finally, the emergence of new trends in the military’s economic involvement and management is, to a considerable degree, the consequence of Egypt’s tightening fiscal conditions. Its economy has been repeatedly buffeted by external shocks since 2020: the COVID-19 pandemic, followed by the start of the Ukraine war in 2022, the Red Sea conflict in 2024, and the U.S.-Israeli war on Iran in 2026. Indeed, it was the Ministry of Defense, not the Cabinet Office or any other civilian agency, that issued a slickly produced YouTube video in April 2026 explaining to the public why the government had instituted energy conservation in order to shield the economy from the latest Gulf war.11

These geopolitical and geoeconomic shocks appear to have prompted the Sisi administration to strive for greater efficiency in military-managed economic projects in recent years, but in order to double down on a flawed approach rather than reconfigure it. However, tightening fiscal conditions also account for an intensification of familiar rentier patterns and relationships among all market participants. The Sisi administration is caught between a chronic shortage of public finances and its political need to purchase loyalty by widening the circle of patronage. With his final term in office ending in 2030, the president must also maintain the political support of the armed forces if he is to seek a constitutional amendment enabling him to run for an additional term, which he appears set to do. It is the centrality of the armed forces to the president’s power, rather than a rigorous cost-benefit analysis of their economic function or of the pattern of state investment, that ensures they will further deepen their role as the backbone of Egypt’s economy.

The political supremacy of the president and the armed forces explains why the Egyptian military is involved so extensively in the national economy. Its control over state institutions, coercive apparatuses, and regulatory authorities is systematically translated into opportunities for rent extraction, asset monetization, and the consolidation of patronage networks. However, further questions arise regarding the particular economic model the military follows, above all why has it emerged in this particular form? What are the model’s true economic and financial costs and benefits? And how are these affected when social and environmental impacts are factored in?

Crucially, the military’s activities have not emerged as a state response to market failure. The military has not stepped in where the private sector was absent, compelling the state to lead with venture capital or to prepare conditions for market entry by other actors. The private sector already held a dominant position in almost all economic sectors in which the military has established its own businesses and activities.12 This encompasses construction and real estate development, a wide range of civilian manufactured goods from cement and steel to household appliances and solar panels, retail services, contracting, food supply and imports, quarrying, fish farming, hospitality and tourism, agriculture, and even desert land reclamation.13

Similarly, Sisi has often pointed to the creation of infrastructure on a scale that the private sector could not afford or would not undertake of its own accord, and to the investment opportunities this offers. But the nature, scale, and pace of these schemes are determined entirely by him, without consultation with the private sector. Twelve years into the Sisi administration’s big push to attract private investment, the continuing lack of a legal framework governing business relations between civilian investors and the military, which is often the landlord in public-private partnerships, acts as an added disincentive. In any case, it is private contractors who deliver the actual construction of infrastructure and housing, albeit under military management. If the private sector is capable of undertaking work on this scale, then the real question is why the state would invest so massively in construction projects that exceed actual demand? With the actual population of new cities a mere fraction of official targets, for example, associated infrastructure such as highways and desalination plants are severely underutilized.14 For example, a relatively popular coastal destination such as New Alamein has only an estimated 20 percent occupancy even during the high season, and therefore a proportionately low rate of use of its desalination plant.15

The critical element shaping the model of military involvement in the economy is that it reflects a political economy of power. On the one side, certain military agencies drive the president’s agenda of income generation through large-scale projects and monetization of state assets, while others maintain the loyalty scheme that evolved from the 1990s onward and sustain the military’s vested interests. On the other side, the model offers clear rewards for large and medium businesses that participate in military-managed projects and that may then ride the wave by setting up their own ventures in the same sectors, most prominently in real estate development. This works well for politically connected private businesses, including some directly affiliated with military or intelligence agencies, but it does little to stimulate production and productivity across the rest of the real economy or encourage private-sector development and autonomy.16 The strikingly low share of local content in manufacturing, estimated by the minister of investment to be 20–40 percent as of April 2026, underlines this.17

The effects are far-reaching. The model exerts a crucial impact on the broad policy framework and market conditions in which other economic actors operate, skewing market signals and incentives for all participants. The military, in particular, has considerable leverage. It imposes measurable impacts on the terms of market participation for private actors thanks to the sheer scale of the projects it manages, and enjoys access to debt-based financing, severely reducing the private sector’s access to domestic credit markets. And by designating state land for new cities or other projects, the military drives up the value of the land, enabling it to be sold for larger sums.18 It thus biases the structure of the economy and the overall investment map.

To be meaningful, any cost-benefit analysis of the military-managed parts of the state-led investment strategy must take all these factors into account. Too often, military-managed projects are chosen and evaluated individually, on the basis of their installation and production costs and expected cash return. There is inadequate or no accounting for future maintenance and periodic rehabilitation, or of impacts on other market actors, or of the costs of borrowing that the government must incur in order to fund projects.19 Similarly, knock-on effects in terms of stimulating upstream or downstream activities and investments for the wider economy are rarely considered beyond the short term, if at all. A foremost example is job generation and skills development: labor engaged in military-managed projects is by far mostly temporary and low-skill, an important indicator in a country where informal employment accounts for around 67 percent of all jobs, which reflects the inadequacy of job-generation in the formal economy.20

Urban real estate development offers a foremost example of these patterns, as it is both the recipient of a major share of public debt-based financing and has been marketed by successive governments as an engine of growth. However, Alternative Policy Solutions, a policy research project based at the American University in Cairo, argues:

Real estate attracts investment as a store of value rather than a productive or sustainable source of growth. Capital inflows into the sector are temporary and finite, after which real estate ceases to produce any value. Construction jobs, which are touted as another form of economic growth linked to real estate, tend to be temporary, low-skilled, and underpaid, contributing further to informality and financial insecurity. As for the potential tax yield, real estate taxes in Egypt remain low. Despite recent amendments to Egypt’s tax regime, real estate wealth tax revenue will account for only 0.1% of annual revenue in FY2025/26.21

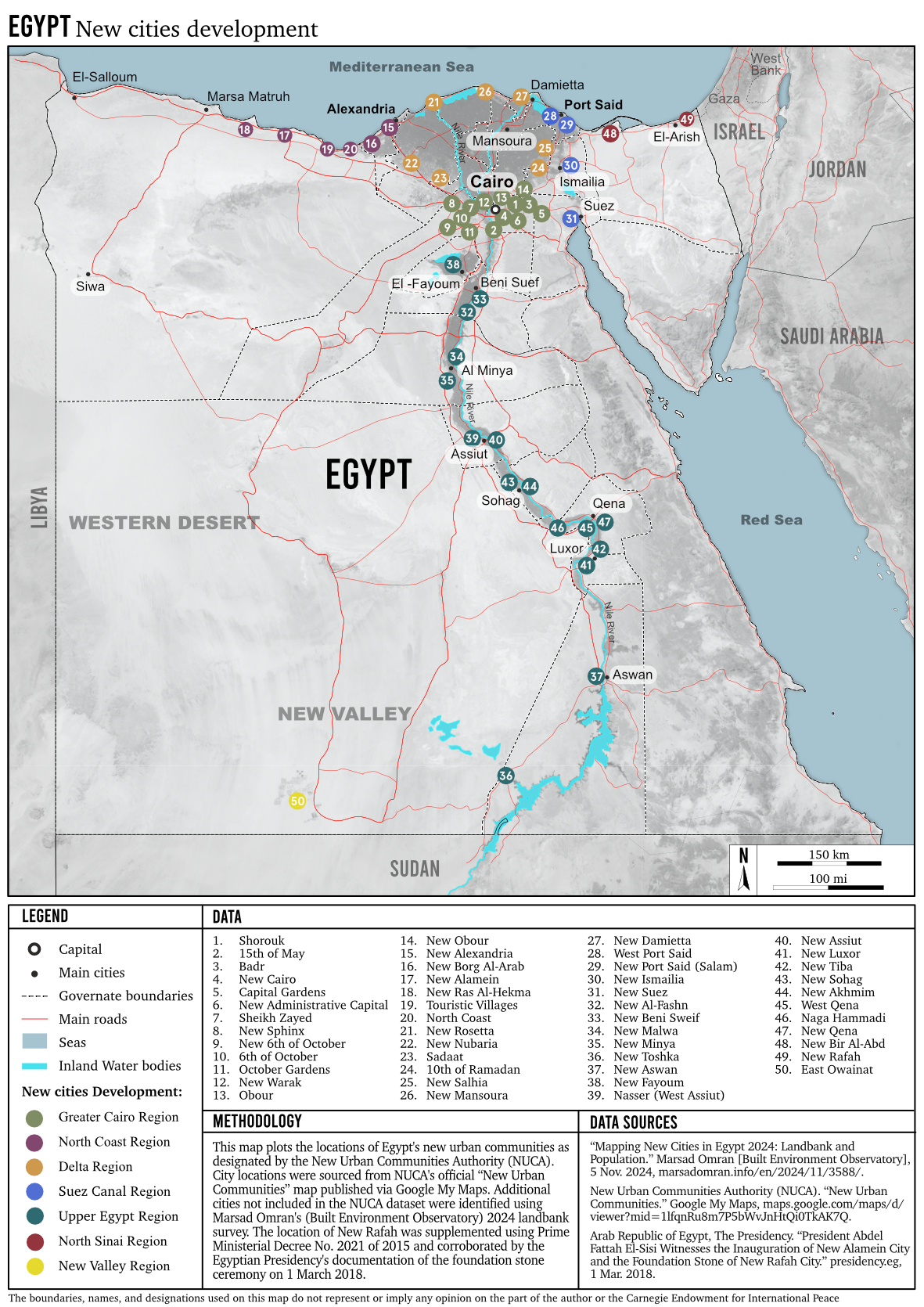

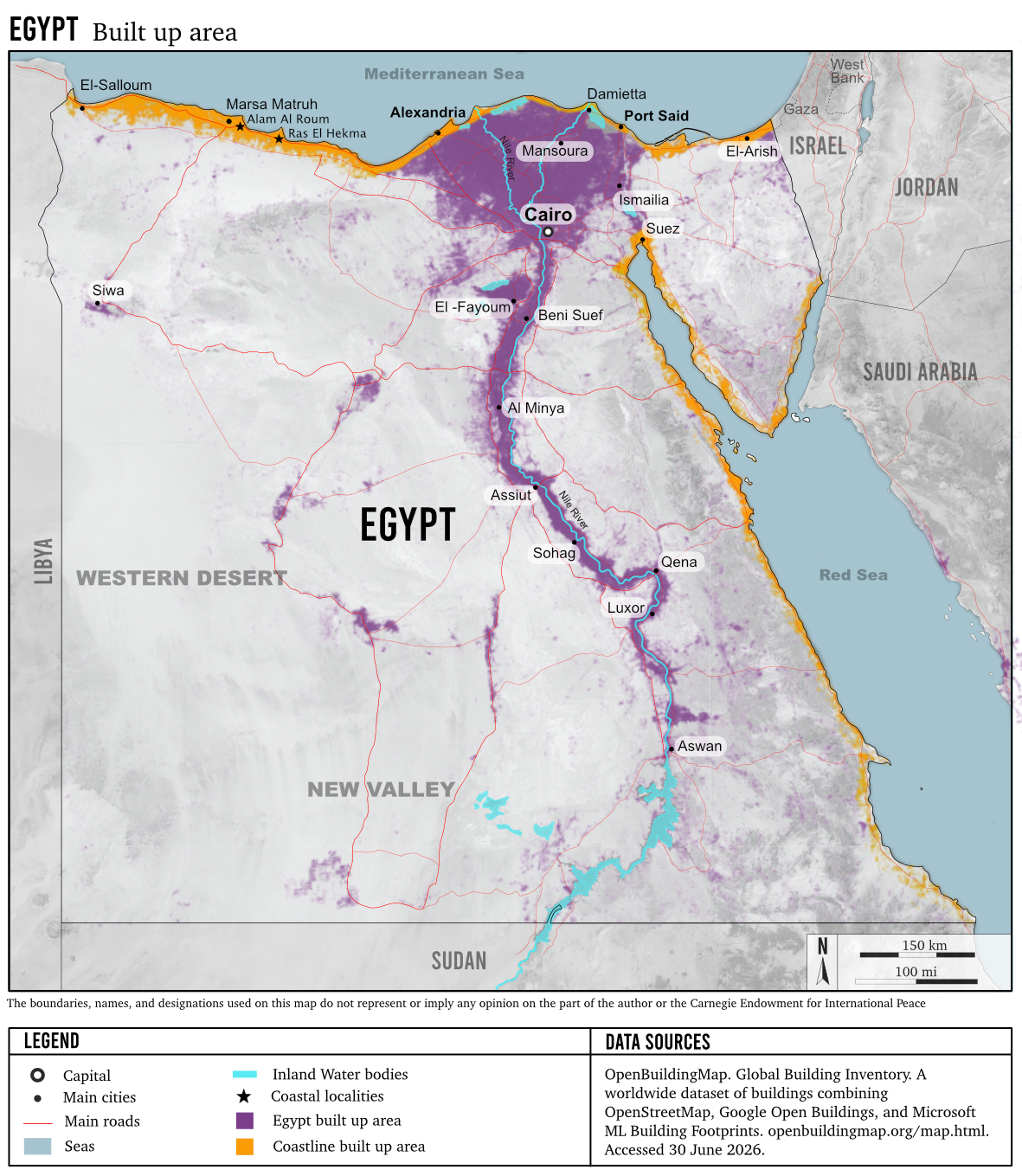

Indeed, the data show both that overall housing supply exceeds demand and that 88 percent of all new housing delivered by the public and formal private sector is built in the new cities.22 Furthermore, as of mid-2024 there already were forty-nine new cities of all categories, mostly constructed under military management but coming under the administrative responsibility of the New Urban Communities Authority (NUCA), with a total population of only 1.7 million.23 This is apart from two cities constructed by the Armed Forces’ Engineering Authority, and others constructed by private developers. In other words, the new cities serve almost entirely to store value for Egypt’s middle class, whether living at home or abroad, diverting capital into non-productive uses. Notably, the military agencies involved in urban real estate schemes shift the financing burden onto the banking sector, which lends developers the funds needed for actual construction.

Financial cost-benefit also cannot be measured or verified for military-managed projects, as the relevant data is kept behind a firewall that applies to military activities in all domains, including the civilian domain, in the name of national security. Overall allocations may be known for government-funded projects, but not for projects managed by parastatal bodies or programs that report directly to the president; the former are included in the general state budget, the latter are not. In both cases, the breakdown of spending, the share of official budgets going to private contractors in military-managed projects, and items such as arrears through which full costs are obfuscated, are also not revealed. This obscures in particular the amounts taken by the military as management fees, which are not based on an official or fixed scale but are known by government and business insiders to range from 5–35 percent of project budgets.24 This is additionally significant because project budgets are not revised to reflect fluctuations in the prices of materials or in the cost of obtaining foreign exchange to pay for imports, compelling private contractors who do the actual work to cut into their own profit margins, or even to incur net losses in order to deliver projects.

Environmental impacts represent another missing element in assessing costs and benefits in military-managed projects.25 Large-scale construction of housing and infrastructure, massive desert land reclamation and cultivation, manufacturing, mineral extraction, and fish farming are energy- and water-intensive. The same is true of urban regeneration schemes that aim primarily to increase cash revenue; these are estimated to have reduced green spaces in Cairo by approximately 95 percent in the eight years up to 2024, for example.26 All military-managed projects have potentially significant environmental impacts, including carbon emissions, air pollution, water contamination and depletion of non-renewable aquifers, and soil degradation. And yet Egypt’s transition to sustainable energy resources has been minimal. To take one measure, the amount of electricity generated from renewables reached only 14 percent by 2025, barely changing from a decade earlier and far short of the targeted 48 percent by 2028, while only 2.2 percent of the country’s energy consumption was clean and its carbon-dioxide emissions increased by 142 percent in 2000–2023.27

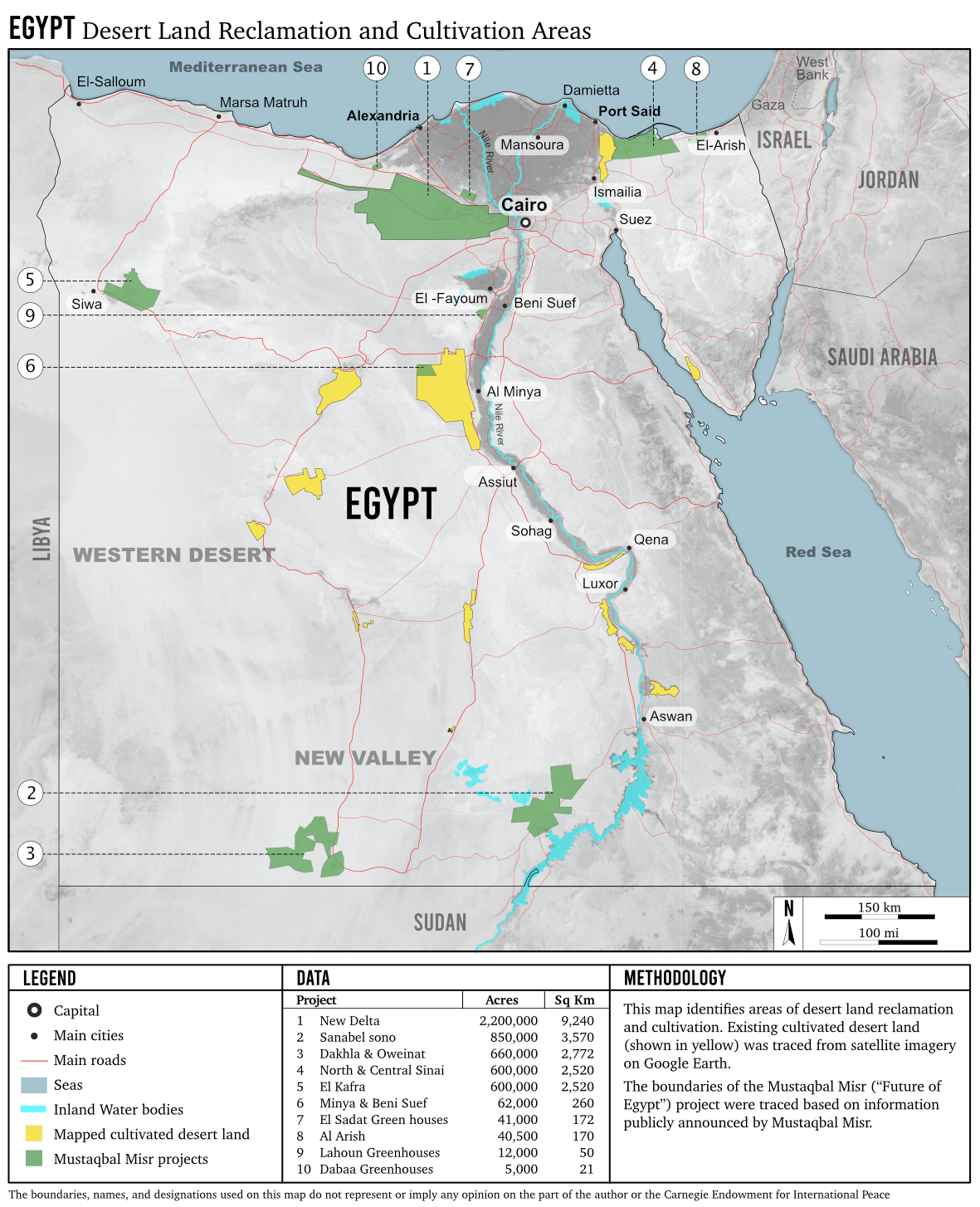

The potential scale, and therefore impact, of these risks is demonstrated by the Egyptian Air Force’s Future of Egypt Authority for Sustainable Development, or Mustaqbal Misr, which manages half of Egypt’s total cultivated land and plans to increase the total from 9 million to 12 million feddans (12.45 million acres) by the end of 2026.28 This has material implications for an ecosystem (population, agriculture, and water resources) that is already under severe strain due to global climate change. But although military officials routinely adopt a “green” discourse, military-managed activities in the civilian domain are kept behind the same informational firewall as financial data, making it impossible to independently assess their environmental impacts and raising the potential cost of remedial action that may become necessary in future.

Social cost-benefit analysis is no less necessary, in particular, of military landlord capitalism. The emphasis on undertaking large-scale projects on the grounds of attaining greater efficiency in production emulates global patterns. In Egypt it is especially evident in state-funded agricultural schemes, notably in desert land and hothouse cultivation, which are all now military-managed, accounting for an estimated half of all land under cultivation.29 Entry investment thresholds permit only large leaseholders, while the military’s unchecked power to expropriate water resources and divert foreign exchange to fund its projects further squeezes out or bankrupts small farmers and dairy producers. Small farmers, who are predominant among the 20 percent of the population who work in agriculture, have also been pushed to bare subsistence farming or off the land due to the invasion of drainage from large land reclamation and cultivation schemes.30 Fishing communities on Egypt’s lagoons and inland lakes have been similarly affected as military landlord agencies reset usufruct fees and catch sizes and run their own large-scale commercial fish farming and minerals extraction ventures.31 Bedouin and other rural communities have additionally been repeatedly dispossessed in northwest Egypt to make way for real estate developments, including fourteen new cities, major resorts including the enormous Emirati- and Qatari-funded Modon Ras El-Hekma and Alam al-Roum schemes, and transport infrastructure.32

The social impacts of military landlord capitalism are no less significant for low-income populations in urban areas. An estimated one-third of Egyptian households live in a deprived built environment, measured against standards for adequate housing, affordability, durable housing, secure tenure, sufficient living space, and safe water and improved sanitation.33 Military-managed projects have removed hundreds of thousands of the poorer residents who account for the 60 percent of the population of the greater Cairo region living in informal settlements, and have destroyed cultural heritage sites, to make way for upmarket residential and commercial developments and for transport networks.34 Drawing on official government reports, urban researcher Omnia Khalil estimates that 1.7–2.8 million people, or 14 percent of Greater Cairo’s population, had been displaced by 2024.35 Displaced residents are offered replacement housing in new locations that are often remote and distant from their markets. Khalil moreover calculates that replacement housing is far below the volume needed to rehouse the numbers of people suffering eviction and relocation, indicative of the paradox in which a significant amount of new housing units remain empty because they target higher income groups.36 Coupled with neoliberal fiscal policies that have slashed subsidies for basic commodities and reduced public education and health services, these practices have contributed to a sharp increase in poverty since Sisi occupied the presidency in 2014, leaving an estimated 33.5–35.7 percent of the population living below the national poverty line.37

A key evolution in the military economy is the rise of military agencies that do not produce buildings or food, but rather manage land as a capital asset. “Value is extracted not through cultivation or the organization of agricultural labor,” rural sociologist Saker al-Nour notes, “but through rent, control over access, and the regulation of who may enter the agricultural sector in the first place.”38 The same may be said of urban real estate under military management, which is the second main form of military landlord capitalism.39 It is in this broad sector of the military economy that the question of maturation versus saturation arises most forcefully, as relatively easy initial gains in profitability may hit up against inherent limitations that are determined by natural resource constraints and a dependency on constant inflows of nonproductive capital from abroad.

Crucially, military landlord capitalism is a direct response to Sisi’s longstanding striving to monetize state assets. This is in contrast to the Sovereign Fund of Egypt, for example, which was established by presidential decree in 2018 and entrusted with generating income from state assets, yet whose performance to date has been lackluster.40 Indeed, the dissimilarity with military landlord agencies extends to other military agencies that have not met the president’s expectations. Most prominently, the National Service Projects Organization, which for years spearheaded many of the Sisi-driven efforts to reclaim desert land, expand food production, and generate revenue from leasing agricultural land to Gulf investors, has largely lost this role to the more successful Mustaqbal Misr.41

Egypt’s military landlord capitalism is enabled by five overlapping factors: First, military control over the use of state land. The Ministry of Defense is one of several government bodies that must approve applications for the use of state land for any civilian purpose, and wields considerable leverage over the National Center for Planning State Land Uses, which governs the use of all state land.42 The military, therefore, acts as a gatekeeper controlling access to and exploitation of state land by all civilian actors, both private and public, granting it considerable fee income and informal leverage.

Second, the award of exclusive economic usufruct. Since 2016, Sisi has designated most, if not all, national highways connecting Egypt’s cities and productive zones as “strategic areas of military importance in desert land,” a legal definition that has also been extended to sections of the Mediterranean and Red Sea coasts, and dozens of Red Sea and Nile River islands.43 This designation effectively awards the Ministry of Defense exclusive commercial franchise over these areas, which it uses to charge private investors for permission to establish businesses or erect billboards.44 As importantly, land in strategic zones may be leased to civilian investors but not sold freehold, leaving the military in control in perpetuity.

Third, administrative leverage. Law 89 of 1998 Regulating Bids and Tenders, which awarded government ministries and agencies extensive power to award contracts up to a certain value and within specific domains by what is commonly known as “direct order”—meaning on a no-bid, noncompetitive basis—conferred the same powers on the Ministry of Defense and other military entities.45 Extensive penetration by military retirees of the state bureaucracy provides the military with additional informal influence over the awarding of contracts, licensing, customs clearance, and, in the case of civilian companies operating in strategic zones or more generally in desert land, supply of labor, water, and other needed materials, further amplifying military leverage over private entities and businesses. An additional trend in recent years has been the transfer, on presidential or government orders, of the jurisdiction and assets of general economic authorities to military control, including the General Authority for Rehabilitation and Agricultural Development, the General Authority for Fish Resources Development, the Arab Land Reclamation Company, the Lakes and Fish Resources Protection and Development Agency, the Sinai Development Authority, and branches of the Agricultural Research Center.

Fourth, the shielding of military agencies and activities from civilian law and courts and, conversely, the extension of military jurisdiction into the civilian domain. Business or ownership disputes cannot be resolved in civilian courts, leaving civilians, including private investors, dependent on personal or political connections, or on bribes, to protect their interests as well as to secure subcontracts in the first place. As importantly, the military agencies assuming the jurisdiction of civilian economic authorities, such as the ones listed above, refer claims against their lessees to military courts, which apply the rules and regulations of those authorities. The blurring of boundaries between the military and civilian domains has been reinforced by the integration of military courts into the civilian judiciary, with the post of deputy head of the Supreme Judicial Council currently being held by the head of the military justice system. Military courts additionally try civilians for “crimes that harm the basic needs of society relating to food commodities and products,” according to Law 3 of 2024, which moreover grants full judicial powers of arrest and investigation to designated military personnel.46 In parallel, by asserting direct presidential control over the country’s main audit agencies and exempting the military from their remit, Sisi has extended the military’s economic reach and shielded its income and investments from scrutiny.

Fifth, military agencies are able to shift much of the burden of financing schemes onto state-owned banks, which provide private real estate developers with a mix of direct loans and of underwriting. NUCA, which although not a military agency is a principal partner in large-scale real estate projects, accounts for an additional portion of borrowing, reportedly owing 150 billion Egyptian Pounds (some $3 billion) in debt to the state-owned National Bank of Egypt (Al-Ahly) and Misr banks by late 2025.47 This has left state-owned banks holding a large part of the country’s real estate portfolio and the associated risk, which is ultimately secured by the state treasury rather than by the military agencies involved in the construction and management of the real estate projects. Concern over contingent liabilities is partly why the International Monetary Fund introduced a new emphasis in its July 2025 review of the current loan agreement on the role of the Central Bank of Egypt, seeking to place it at arm’s length from public banks and to convert it into a shareholder rather than owner of state assets.48

Sisi evidently regards the creation of urban real estate as a foremost means of generating state revenue and of driving economic growth. This is created in two ways: by building dozens of new cities on desert land, and by transforming public spaces and low-income neighborhoods into prime locations for commercial development in “old” cities, primarily Cairo and Alexandria. The fact that the state holds some 94 percent of all land, and that the real estate sector is estimated to account for 20–30 percent of GDP, makes the creation of prime urban real estate a centerpiece of Egypt’s landlord capitalism.49 Egyptian officials have even coined the term “real estate exports” to blur the speculative nature of real estate development.

Seen in isolation, the monetization of state land in urban and rural areas, former U.S. intelligence official Amir Asmar argues,

reduces unsustainable borrowing, brings in valuable foreign exchange, develops underutilized land, imports managerial expertise, and helps stabilize currency. The immediate cash flow is crucial for Egypt’s balance-of-payments management and is supplemented with long-term profit participation and tax revenues. . . . However, the proceeds are typically used to finance current obligations or other investments; they do not necessarily reduce existing debt unless explicitly designated for debt repayment, which is planned for only some of the generated revenues.50

Predictably, given its central role in Sisi’s economic approach and in the allocation of state land, the military leads the process of creating urban real estate and of managing it as lessor and landlord. While the latter terms overlap, in some instances the military has the power to lease land under its control, land it does not, strictly speaking, own; in other cases, for example where land is designated as “private domain state land,” the land may be regarded as “owned” by the military, effectively making the institution a landlord and entitled to its income. Crucially, by classifying construction projects as “national,” the president and the government sidestep the need for a tendering process and shift construction, demolition, and licensing powers from local authorities to the implementing military agencies. This was demonstrated in Cabinet Decree 38 of 2026, which allocated the construction of a yacht marina on Egypt’s northwestern coast to the Armed Forces’ Engineering Authority, for example.51 Placing projects under management of the military, moreover, means that any purported crime or dispute in, or pertaining to, its areas and facilities falls under the jurisdiction of the military prosecutor’s office.

The military has managed the construction of dozens of new cities, housing in old cities, and associated infrastructure. Military agencies managed 25 percent of publicly funded construction in 2013–2018 (including transport and agriculture as well as housing), rising to 28–38 percent in 2019–2020.52 The military is reported by highly placed government and business insiders to levy management fees of 5–35 percent, which it withholds from project budgets.53 With the construction sector accounting for 15 percent of Egypt’s GDP overall, both the military’s role and its income are considerable.54

The scope for further growth in this sector was dramatically highlighted by the massive Modon Ras El-Hekma luxury real estate development scheme on the north coast funded by a $35 billion investment from the United Arab Emirates (UAE) in 2024, and a similar Qatari-funded scheme worth $29.7 billion at Alam al-Roum, concluded in 2025.55 Private developers heavily invested in military-managed real estate projects are benefiting from the favorable policy environment to launch their own large schemes. A foremost example is Hisham Talaat Moustafa, regarded as a go-between connecting the UAE, the military, and the Sisi administration. In 2024, he launched SouthMED, a 1 trillion Egyptian pound ($21 billion) tourism project, also on the north coast, and in 2026 he announced the launch of a 1.4 trillion Egyptian pound ($27 billion) city called The Spine to the east of Cairo.56

Multiple military agencies are involved in developing urban real estate. The Armed Forces’ Engineering Authority is the lead agency in managing construction of government-funded housing (mostly high-end) and public infrastructure. It delivered between 27.5 percent and 38 percent of all publicly funded civilian construction projects in 2014–2020. The authority has not issued comprehensive statistics since 2020, but Sisi’s statement in October 2024 that the state had spent 10 trillion Egyptian pounds ($323 billion) on projects in the first decade of his presidency indicates the potential military share.57 The Engineering Authority and the Ministry of Housing’s NUCA have together launched construction of twenty-four so-called smart cities since Sisi came to power, almost all aimed at upmarket customers. Government statements vary, but the plan is to take the number of new smart cities up to thirty-eight by 2050, with a projected population of 32 million.58 A newcomer military agency, the Air Force’s Mustaqbal Misr (discussed in the next section), has also formed a joint company with the Ministry of Housing to manage, maintain, and operate new cities, and is even building six new cities of its own. 59 The construction of new cities assures the military of a seemingly endless income stream, whether or not these cities are inhabited to capacity. Real estate schemes, especially those conducted in partnership with Gulf investors, may additionally offer a means for the military to recycle its income.

In parallel, the Armed Forces Land Projects Agency (AFLPA) has emerged in recent years as an important military vehicle for monetizing the state’s real estate portfolio in “old” cities and in a handful of new cities: the upmarket Galala city on the Red Sea coast and New Ismailiya city on the Suez Canal, and, most significantly, the country’s New Administrative Capital.60 The Ministry of Defense owns a 51 percent stake in the Administrative Capital Urban Development Company (ACUD), which is managing the new capital project at a cost estimated at launch of $45 billion.61 AFLPA holds 21.6 percent of the military share in ACUD, with the National Service Projects Organization (NSPO) holding the remaining 29 percent, and both therefore receive shares of the rent paid by government ministries and agencies moving to the new capital and by private investors purchasing leaseholds there.62

The drive to monetize prime state-owned real estate has included replacing inner city low-income neighborhoods with upmarket high rises, as occurred in the Maspero Triangle and on Warraq Island in Cairo, and in Alexandria. As part of the drive, Prime Minister Mostapha Madbouly transferred management of the so-called Shubra-Helwan corridor along the Nile River from the Ministry of Irrigation to AFLPA in 2020, which empowered it to collect rent from residential and commercial moorings and enterprises on mid-river islands along a 44-kilometer (28-mile) stretch in the Greater Cairo region.63 AFLPA subsequently auctioned off commercial leaseholds in its area of management along the Nile in Cairo for recreational and hospitality ventures.64 Spaces previously designated for “public benefit” in Cairo and Alexandria—parks, agricultural research centers, and government employees’ social clubs—were also transferred to the Ministry of Defense for upmarket residential and commercial investment projects.65 Even the Ministry of Military Production was awarded a twenty-five-year usufruct contract to rehabilitate the Giza Zoo and Orman botanical garden.66

Monetization of public spaces and state land extends beyond traditional built-up areas. As noted earlier, successive presidential decrees have designated many areas as “strategic zones of military importance,” placing them under the Ministry of Defense’s control.67 Much of this designation is done to prevent encroachments on state land, as was the case for the award of thirty-six mid-river islands in the Nile in 2022, at least some of which are intended for commercial development.68 On highways, the ministry levies tolls and charges for the establishment by private companies of service stations, other facilities, and advertising billboards.

The Ministry of Defense has exploited the difficulty of private investors to access land under its control by constructing military-owned hotels in prime tourism locations: for example on Tawila Island and Al-Gamsha in the Red Sea, the Regal Heights and the Crystal Inn in New El Alamein on the Mediterranean coast, and the St. Regis in the New Administrative Capital.69 Military-owned hotel chains Triumph and Tolip have also continued to expand, with Tolip buying a luxury hotel in Sharm al-Sheikh in March 2023.70 Government-funded conferences are routinely held in military-owned hotels, assuring them of income.

Mustaqbal Misr is another showpiece for Egypt’s new form of landlord capitalism. An affiliate of the Egyptian Air Force, the agency was established by presidential decree in 2022, and was described by the official State Information Service a mere two years later as “one of the largest development entities in the world.”71 Its appearance reflects the belief among Egypt’s agricultural policymakers that large-scale farming and agribusiness in reclaimed desert land is more effective for feeding the country.72 Accordingly, the purpose of Mustaqbal Misr is to “increase the agricultural area in Egypt, achieve food security and provide job opportunities within the framework of the State’s vision for sustainable development,” and also to partner with “serious agricultural investors.”73 The presidency describes the agency as the first new reclamation project to “achieve self-sufficiency and export the surplus,” highlighting the effort to reduce food imports, save foreign exchange, and generate revenue from exports.

Mustaqbal Misr’s primary approach is to lease desert land, by definition state-owned, to private investors for cultivation, while retaining overall control and management. This follows reclamation of the land and construction of basic infrastructure, including roads, electricity plants and distribution networks, and water supply, which is conducted by Mustaqbal Misr, the Engineering Authority of the Armed Forces, and other government entities. Egyptian landlord capitalism differs in these two key respects from, say, the Ethiopian or Sudanese version, where large tracts of land are leased to foreign investors for exploitation without significant preparation or management by national authorities.

Much, if not all, of publicly reclaimed desert land has been placed under Mustaqbal Misr’s management, which left it in charge of “leading and supervising half of Egypt’s cultivated land” by early 2025, according to a media outlet affiliated with the General Intelligence Service.74 The agency’s executive director, air force pilot Colonel Bahaa el-Ghannam, claimed it had contributed $4.3 billion in import substitution and exports of crops in 2018–2024, and generated 40,000 direct and 2 million indirect jobs in 2024 alone.75 He anticipated generating 80,000 direct and 3.5 million indirect jobs by 2027, and reaching annual returns of $3.7 billion in import substitution and $2 billion in exports annually by 2029.

Mustaqbal Misr has also taken on other aspects of managing Egypt’s food supply. Most importantly, it assumed responsibility for commodities procurement from the General Authority for Supply Commodities in 2024, becoming responsible especially for procuring wheat for Egypt, which is one of the world’s largest importers.76 Two years later, Sisi assigned Mustaqbal Misr exclusive control over rice exports and the revenue they generate in foreign currency. The agency is now regarded as one leg of the country’s “food security triad,” formed with the ministries of agriculture and irrigation and of supply.77 Mustaqbal Misr’s position in Egypt’s food supply was reinforced by its acquisition of a majority stake in the state-run food commodities exchange in July 2025, which oversees trade in crops and agricultural production inputs, including pesticides and fertilizers, and its purchase of shares in several private companies and publicly listed government entities operating in the food, land reclamation, and tourism sectors.78

Mustaqbal Misr subsequently deepened its role in domestic food trade and distribution by establishing its own “Super Tawfeer” (Super Savings) retail chain, intended to provide food from farm to table and reduce prices by cutting out intermediaries.79 But it almost immediately subsumed this chain under the new and much larger Carry On brand, which it oversees on behalf of the government.80 Designated by Sisi as a national project in February 2026, Carry On brings together some 50,000 retail outlets and subsidized food ration distributors belonging to the Holding Company for Food Industries and the Micro, Small, and Medium Enterprise Development Agency, cumulatively serving 60.8 million customers.81 In parallel, Mustaqbal Misr has also constructed massive storage facilities, launched a dairy plant to produce baby formula, and is setting up solar energy farms.82

The agency’s meteoric rise reflects vigorous support from Sisi, who frequently includes Ghannam in economic leadership meetings. A measure of Mustaqbal Misr’s status is its takeover of projects previously run by the NSPO, including desert land reclamation, management of coastal lagoons and inland lakes that are sites of fish farming and mineral extraction, animal breeding, and building maintenance and cleaning. Similarly, the agency has displaced the Sons of Sinai company as the country’s largest conduit for rice exports. Sons of Sinai is owned by Ibrahim al-Argany, a close regime affiliate who probably represents the commercial interests of Military Intelligence. Therefore, the loss of its market position again suggests powerful presidential support for Mustaqbal Misr.83 Reflecting growing confidence, Mustaqbal Misr’s Ghannam has suggested it would offer shares to private investors in the Egyptian stock exchange—something the NSPO has been supposed to do since at least 2020—although this has yet to materialize.84 Indeed, Mustaqbal Misr’s official website remained under construction as of July 2026, underlining its opacity.85

Mustaqbal Misr has since diversified into non-agricultural activities, a sign of the political backing it enjoys and, consequently, of its ability to tap into financing and attract private-sector partners. This is illustrated by its construction of an upmarket private city and special investment zone, Jiryan, through its new property arm, Nations of Sky, which claims the project will involve investments worth 1.5 trillion Egyptian pounds (approximately $31 billion).86 Nations of Sky also claims to have five additional new cities in production or “coming soon.”87 Through its Modon Misr subsidiary, Mustaqbal Misr will additionally “manage, maintain, and operate buildings, urban communities, and infrastructure . . . alongside overseeing cleaning services” in the dozens of new cities constructed with public funds nationwide over the past few decades. Most of these cities target an upper-middle-class clientele and middle-class families seeking a safe haven for their savings amid surging inflation.88 With the number of new cities set to increase over the coming decade or more, Mustaqbal Misr stands to extend its position in newly created urban real estate.

Mustaqbal Misr is clearly on the rise. Indeed, Sisi drafted a law in July 2026 redesignating the agency as a special economic authority under his direct control, exempting it from government regulations and taxation, and empowering it both to set its own salary scale and profit-sharing scheme and to establish two sovereign wealth funds to invest its income.89 The potential expansion of its remit is extraordinary: In addition to agriculture, which includes animal, poultry, and fish production, its scope will include mineral extraction, logistics, tourism, construction, energy, water, education, electricity, and communications and information technology.90

Although the new law nominally transforms Mustaqbal Misr into a civilian state body, its accounts remain hidden behind an information firewall, as with all military agencies involved in any aspect of delivery of civilian goods and services. This prevents verification of its claims of profits or a cost-benefit assessment of its business model. Contradictory statements about the cost of reclaiming desert land in the New Delta scheme, which is under Mustaqbal Misr management, offer an example of this problem. The official website of the Egyptian presidency gave the total cost of preparing 1 million feddans (1.038 million acres) for cultivation as 8 billion Egyptian pounds (approximately $160 million), whereas Sisi himself has claimed that the cumulative cost for the same surface area came to around 200–250 billion Egyptian pounds ($4.2–$5.27 billion).91 This is apart from the cost, so far undeclared, of constructing a 500-kilometer water transport network (including a 170-kilometer man-made river) to irrigate the scheme.

The military economy extends well beyond the real estate and agriculture sectors, to include manufacturing, retail trade, food production and packaging, contracting, mineral extraction, and various services including IT management, hospitality, and protection. In all, these activities constitute some 91 percent of all military production of goods and services in the civilian domain.92 The bulk is conducted by bodies that have been formally registered as companies, whether under one or another public-sector company law or through the simple process of company registration at the local chamber of commerce. This sets them apart from other military agencies involved in urban real estate development or land reclamation and cultivation, which are direct affiliates of the Ministry of Defense or branches and departments of the armed forces.

Although around a hundred military companies now operate in these sectors, their market share in most of them is modest, if not entirely negligible.93 And with the exception of the steel and cement sectors specifically, military companies do not shape any economic sector as a whole in the way that AFLPA and other military agencies shape urban real estate or Mustaqbal Misr shapes agriculture. Furthermore, although financial data relating to their operations and turnover are either not released or else known only in their broadest detail, it is likely that the collective net income of military companies is considerably less than the income accruing to the military agencies engaged in landlord capitalism. Indeed, a number of military companies are known to be loss-makers, with the state treasury subsidizing their losses. Even for those that claim net profits and growth, these are due to their privileged market in military-managed projects—especially construction—and to their assured supply of public procurement contracts, many of which are awarded by no-bid direct order.

The fact that military companies have more than doubled in number since 2013 reflects not market performance, therefore, but the political primacy of the military in what Sisi has called Egypt’s “new republic.”94 For several decades prior to this and until several years into the start of Sisi’s presidency, the common justification for the involvement of military companies in civilian markets was that they were merely utilizing surplus production capacity in factories and farms that had originally been established to meet defense needs. But approximately three-quarters of all military companies, including all the new ones established since 2013, produce only civilian goods and services, completely undermining the claim of using surplus capacity.95 Along with the fact that only a quarter of the two-dozen companies belonging to the Ministry of Military Production, to take a known example, were profit-making, while another quarter were loss-making and half merely broke even as of 2019–2020, this underlines the extent to which Sisi has empowered the expansion of military ventures politically and legally, regardless of their actual commercial performance or viability.96

The president clearly sets far greater store in the military agencies rolling out landlord capitalism than in the military companies. He has not expanded the authority of the latter or the assets under their control, and none of them are the president’s champions in the way that Mustaqbal Misr is. The three main conglomerates—the Ministry of Military Production, the Arab Organization for Industrialization, and the NSPO—enjoy autonomy to lobby government ministries for contracts, set up new companies or joint ventures with Egyptian and foreign companies, and sit on government boards that vet public procurement or debate strategy for industrial development and other policy areas. But this does not alter the fact that they are a legacy facet of the military economy that has been overtaken by military landlord capitalism. They moreover represent only around 10 percent of the total number of state-owned enterprises, economic authorities, and service authorities that deliver civilian goods and services in various economic sectors.97 In short, the residual military economy functions mainly as a vehicle for elite circulation among the senior officer corps and a means of underpinning their loyalty to the president and regime as a whole.

Because economic viability is not essential, military companies reveal several shortcomings. Manufacturing companies belonging to the Ministry of Military Production and the Arab Organization for Industrialization have formed a number of joint ventures and partnerships with domestic and foreign private companies, but a significant part of their contribution to joint equity consists of providing access to the state land needed to establish facilities and of bureaucratic facilitation. Assembly under license remains dominant, limiting local content and value added. It is also true that in many cases, military companies that win contracts to supply government ministries with particular goods merely import them, rather than produce them locally.

These limitations are demonstrated in two areas. On the one hand, the defense industry has seen some improvements, such as the development of smaller, cheaper systems such as unmanned aerial vehicles and the refitting of existing systems with enhanced electronics. But the underdevelopment of the defense industry as a whole continues to be reflected in a near-total lack of exports (bar the sale of the Fahd wheeled armored infantry vehicles to a couple of West African countries). On the other hand, repeated proposals to relaunch the country’s anemic car industry have failed to take off. The ambition of the Egyptian government and military companies to rival Morocco’s success in becoming an automotive manufacturing hub (not to mention the rapidly evolving Moroccan aerospace sector) remains hobbled by the lack of basic prerequisites, including investment in research and development, effective industrial strategies, and private sector participation.98

All this points strongly to a political economy that favors companies that would otherwise struggle to compete, let alone survive, in a free market. This helps explain the frequent duplication of activities among military companies, and other inefficiencies. It may also explain why repeated official proposals since at least 2018 to offer shares in companies belonging to the NSPO, and more recently in the Administrative Capital Urban Development Company, have not materialized, with a single, partial exception finally reached in June 2026.99 Missing deeds of title to land, murky procurement contracts, opaque bidding, inconsistent book-keeping and pay scales, and other problems are believed to prevent proper financial disclosure that is required for flotation, but a more fundamental obstacle may be military reluctance to relinquish cash cows.100

The problematic incentive structure of the residual military economy is reflected in various ways. On the one hand, individual officers exploit their leverage to extract board membership or shares of equity in startups, or perhaps open small commercial ventures such as eateries and cafés around officers’ clubs and other military facilities in desirable urban areas such as Cairo’s Zamalek. Ironically, this mimics the military’s official takeover of land belonging to government agencies such as agricultural research centers on the grounds that the land “is not producing income,” which is then converted to cafés and similar recreational facilities.101 Informal officer networks exchange insider information regarding new development plans for state land, enabling speculation and profiteering.102 Individual behavior is replicated at the institutional level: the main branches of the armed forces reportedly parcel out stretches of military-controlled national highways among themselves informally, and levy off-the-book payments from investors seeking to set up franchises there.103

On the other hand, military agencies such as the Ministry of Defense’s Armed Forces Financial Affairs Authority, Administration of Clubs and Hotels, and NSPO—and even the Ministry of Military Production, a manufacturing conglomerate—continue to expand their hotel chains, despite underwhelming financial results.104 This is a crude form of military landlord capitalism, which is also apparent in the authority awarded by the prime minister to the Ministry of Defense to levy tolls at all of Egypt’s quarries and mines.105 And an even cruder form of rent extraction is the levying of extortionary tolls from Palestinian families seeking to escape from Gaza, and from trucks delivering aid into the territory, by companies belonging to the military-affiliated crony businessman Ibrahim al-Argany.106

What is next for the military’s role in the Egyptian economy? Will it be more of the same or new directions, and is either trajectory sustainable? Military production and management of public goods and services in certain economic sectors have been on an expansionary trajectory for over a decade, but this has been predicated on factors that suffer inherent limitations. For one thing, the model that has emerged under the Sisi administration works best where the state already controls critical assets and does not have to negotiate with other actors over access or use. This is precisely why the largest state investments relate to land and water use, whether for construction or agriculture.

Conversely, neither the model’s managers nor the Sisi administration seem able or willing to learn how to enable the rest of the real economy to grow and diversify. One consequence is that Egypt’s economy, along with most military production of goods and services, remains at relatively low levels of innovation, local content, and horizontal integration compared to peer economies. This parallels a broader trend for Egypt, which, according to a report on manufacturing by the Organization for Economic Cooperation and Development released in May 2026, has consistently trailed behind other Middle Eastern and North African economies in terms of integration into global value chains, with the distance between them growing over time.107 As researchers Ahmed Dawoud and Samriddhi Vij have noted, “Egypt remains trapped in a low-value ‘farm and quarry’ export model,” which military involvement is only entrenching.108 This suggests the model cannot be replicated in other sectors, and consequently that its current growth trajectory cannot be maintained indefinitely.

New horizons are therefore limited for the military economy. This may explain attempts by several military agencies to enter African markets starting around 2017, possibly building on Sisi’s promotion of Egyptian-African ties that culminated in his chairmanship of the African Union in 2019–2020. These efforts have remained modest, however, focusing mainly on joint ventures in food and livestock production and on civilian construction in Uganda, Tanzania, and Nigeria. Mustaqbal Misr was reportedly also hoping to set up logistics zones in six African countries in cooperation with the Egyptian Ministry of Trade and Industry in 2025.109

Military agencies have also eyed opportunities in Arab reconstruction markets in Syria, Libya, and Gaza, which potentially offer far greater rewards.110 Only Libya has proven feasible in fact, thanks to its reconstruction market estimated at $111 billion in 2021.111 But although a number of Egyptian civilian companies were awarded Libyan contracts reportedly worth $4.2 billion in 2021, military companies and agencies do not appear to have acquired a significant share.112 The Armed Forces’ Engineering Authority was involved in the reconstruction of the eastern Libyan city of Derna following its devastation by Storm Daniel in 2023, and a construction company owned by Ibrahim al-Argany has also received contracts from the rival authorities of eastern and western Libya.113 But the fact that even these successes were owed to political connections confirms the general inability of Egyptian military companies to achieve notable exports or to enter foreign markets where competition is strong—for example in the Gulf states, which host a large number of Egyptian businesspeople and maintain extensive political and financial ties with the Sisi administration.

The basis simply does not exist for the Egyptian military economy to move in new directions, whether in order to escape the structural limitations of the Egyptian market or to generate new sources of badly needed hard currency. The search for new markets is not an outcome of successful expansion or growing competitiveness. Critically, the model that has been applied in relation to urban real estate and agriculture—successfully in the view of the president and the military—does not appear replicable in other economic sectors, such as manufacturing and services. However, simply remaining on the military economy’s current course runs the risk of diminishing returns. This is partly because the amount of prime land for enormous schemes such as Modon Ras El-Hekma and Alam al-Roum is not infinite. Other projects to which Egypt looks for development and attracting foreign investment and loans, including upmarket new cities and desalination and green hydrogen plants, compete for the same coastal real estate.114 Signs of diminishing demand for new housing units were apparent by mid-2026, revealing the limits of the domestic market and prompting private real estate developers to seek other markets abroad.115 Possibly as a response to diminishing opportunities, or to increased appetite, military agencies and companies have been buying shares in other state-owned enterprises.

Of course, these problems are Egypt’s, not just the military’s. To date, whenever Egypt has made real progress in stabilizing its macroeconomic environment, most notably in 2016 and since 2024, this has been short-lived due to deep resistance to embarking on meaningful structural change. Rentier and predatory behavior have continued rather than diminished.116 This also suggests that although the emergence of buoyant private-sector niches could, in theory, give rise to coexistence between military management of state investments and an increasingly autonomous and influential private sector, it may also, and instead, attract further military attention and lead to renewed attempts to capture equity or rent.

In other countries, capital holders who outgrow their national markets expand internationally in order to grow and compete, but the military economic model in Egypt cannot do that.117 It remains entirely dependent on the continuation of large capital inflows to an economy that does not generate enough domestic surplus to maintain an extractive, rentier economic mode. Egypt received some $200 billion in loans, grants, in-kind assistance, and politically motivated investments from the Gulf and international financial institutions and development agencies in 2013–2024, and another $87 billion in pledged or actual real estate investments, debt write-offs, and new official assistance in 2024–2025.118 The fact that debt servicing is nonetheless still set to consume 64 percent of state spending in the proposed FY2026/2027 budget underscores the extent to which the Sisi administration has doubled down on an economic approach that has failed to invigorate nonrentier sectors of the economy, thereby deepening Egypt’s debt trap.119

In his study of Egypt’s cleft capitalism, political economist Amr Adly asked why the country’s massive and sustained inflows of capital over decades had not translated into higher rates of saving and investment. His answer was that these failings were the “results of institutional arrangements—social, economic, and political—rather than mere structural constraints.”120 Adly was discussing the era of president Hosni Mubarak, but his assessment remains valid today. From this perspective, the characteristic features of the Egyptian economy—including its military component—and its shortcomings reflect the Sisi administration’s internal logic, which is arguably more grounded in the fusion of power and accumulation than any of its predecessors—which represents a high bar indeed.

Accordingly, inefficiencies or policy distortions cannot be corrected through technocratic reforms such as the tax reporting measures and financial disclosure encompassing military companies pledged by the Egyptian government in its loan agreement with the International Monetary Fund in 2022.121 Important as they may have been at one time, these can no longer undo the straddling of political control and economic rent extraction that constitutes the foundation of the Sisi administration’s stability.

The political economy of Egypt in Sisi’s era does not entirely prevent improvements in administrative efficiency that may enhance tax collection or economic returns on certain investments. But any such gains occur against a backdrop in which state bodies that command major public assets and income streams and answer exclusively to the president, are exempt from government regulations, taxation, and audit. These bodies account for a significant portion of the public capital investment that is financed through borrowing that the government raises and services. They remain off-book while leaving the government to deal with creditors and cope with contingent liabilities arising from unexpected geopolitical shocks or global economic crises. The government borrows and repays, the president and the military capture the difference between the inflows and incomes that are actually generated.

Senior Fellow, Malcolm H. Kerr Carnegie Middle East Center

Yezid Sayigh is a senior fellow at the Malcolm H. Kerr Carnegie Middle East Center in Beirut, where he leads the program on Civil-Military Relations in Arab States (CMRAS). His work focuses on the comparative political and economic roles of Arab armed forces, the impact of war on states and societies, the politics of postconflict reconstruction and security sector transformation in Arab transitions, and authoritarian resurgence.

Recent Work

Yezid Sayigh

Yezid Sayigh

Carnegie does not take institutional positions on public policy issues; the views represented herein are those of the author(s) and do not necessarily reflect the views of Carnegie, its staff, or its trustees.

There is a disturbing structural parallel between the old global energy economy and the new green transition.

Angie Omar

This will be the region’s most representative tournament, amid broad changes in its footballing landscape.

Issam Kayssi

Understanding how farmers in the Oued Sahel-Soummam Valley grapple with climate change is essential for addressing the paradoxes through which adaptation, operating at both individual and institutional levels, deepens the region’s vulnerability and erodes the social fabric and agrarian identity that once defined life.

Ilyssa Yahmi

Cairo’s efforts send a message to the United States and the region that it still has a place at the diplomatic table.

Angie Omar

The recent African Cup of Nations tournament in Morocco touched on issues that largely transcended the sport.

Issam Kayssi, Yasmine Zarhloule